The economic news is bad – and will likely get worse – but this is not like the Great Depression!

CFEE04.20.20

Top Concern – Health

During the Coronavirus pandemic, the number one concern on virtually everyone’s mind is their health and avoiding the risk of infection. That concern is well placed and it is what is leading most Canadians to abide by restrictions on their behaviour. The willingness of Canadians to commit to what is being asked of them during this crisis is what we hope will enable us to return to a more normal life sooner rather than later.

Next Concern – The Economy

Second to the health concern, though, most Canadians are worried about the economy – their jobs, incomes, savings, investments, ability to make ends meet, and their ability to achieve the goals they had set for themselves and their families. Consequently, great attention is being paid to the economy – its status, data, forecasts, etc. It is the goal of CFEE to provide plain language and factual information to Canadians to help them understand the economic realities that impact their lives and decisions. We aim to do that at all times – but especially during heightened times of concern and uncertainty. In that regard, we believe there is a need to make an important clarification for Canadians.

Does Another Depression Loom? Some in the Media Would Make You Think So

There is no doubt that these are very difficult times and things could well get worse before they start to get better. Unfortunately, though, some things people may hear about the economy are almost terrorizing. Most in the media are looking to provide factual information to a nation looking for news. But as is sometimes the case these days, with so many sources of information, some are using hyperbole to dramatize news and the economic realities. It is important at this time, perhaps more than ever, for Canadians to focus on information sources that are credible, have proven track records and which regard accurate, clear and responsible information as paramount.

Due to the unprecedented nature of the times, and dramatic changes in the course for our economy, there is some talk of a new Great Depression. As new economic data are released – such as news that “Canada’s GDP will drop by about 9% over this last month” – it is important to distinguish times past from times present when making comparisons. You may hear some speculation that these times could be as bad as, or worse than, those of the 1930s. Let’s consider the challenge of making such comparisons.

This is NOT Like The Great Depression

The problem with making comparisons of today with the past is that, as we always know, it is important to compare apples with apples – and not apples with oranges or any other kind of fruit you care to imagine. This economic experience of today is not like that of the Great Depression, or of any other time in the past. Past economic downturns were largely due to declining demand, or spending, in the economy. This downturn is a “supply shock” resulting from the forced shutdown of much business activity. Therefore, we are dealing with truly unprecedented times. Models and prognosticators that are drawing on historical experience for comparisons and extrapolations and assumptions of what lies ahead, are not adhering to the “apples to apples” law. And we should be very cautious in what we are taking from their conclusions and forecasts. Let’s look at why this is not like The Great Depression.

First Off, What is a Recession?

First, let’s consider a recession. An economy’s health and growth are usually measured by Gross Domestic Product – or GDP. GDP looks at the total value of goods and services produced in Canada. We look at that figure to get a sense of how the economy is doing: Is production rising or falling? Is the economy likely to be creating more jobs or fewer? Is the amount we are producing close to what we can produce, or far from our capacity? That is important information for policymakers who need to make decisions as to whether to give the economy a boost, slow it down, or leave it alone. That is why GDP is a key economic measurement.

“Real” GDP versus GDP

But more specifically, economists focus on “Real” GDP – that is, factoring out higher prices and inflation. That isn’t really a hard concept to grapple with. Let’s consider a quick example.

Suppose that in one year Canada produced $50,000 worth of hockey sticks and that the $50,000 was made up of 1,000 hockey sticks sold at an average price of $50 each. Suppose the next year we find that $60,000 was spent on hockey sticks. That seems as if more sticks must have been produced. But if the $60,000 was made up of 1,000 hockey sticks sold at an average price of $60 each, we see that no more hockey sticks were actually produced. The higher figure was because of the higher prices, not because we produced more sticks.

If we want to know how many sticks were actually produced, we have to factor out the impact of the higher prices, or inflation.

Recession = Two Consecutive Quarters of “Negative Growth”

That is what economists do for the economy as a whole to get a measurement of the total goods and services produced in Canada in a given period of time. Those time periods are usually quarters – or every three months. If the quantity of goods and services actually falls from one quarter to the next, that is a decline in production – or what is somewhat strangely called “negative growth”.

If the level of output in an economy falls for two consecutive quarters, that is the technical definition of a recession. Recessions can vary in length from a couple of months to many months. Recessions can also vary in terms of severity – from modest declines in growth to significant declines in growth.

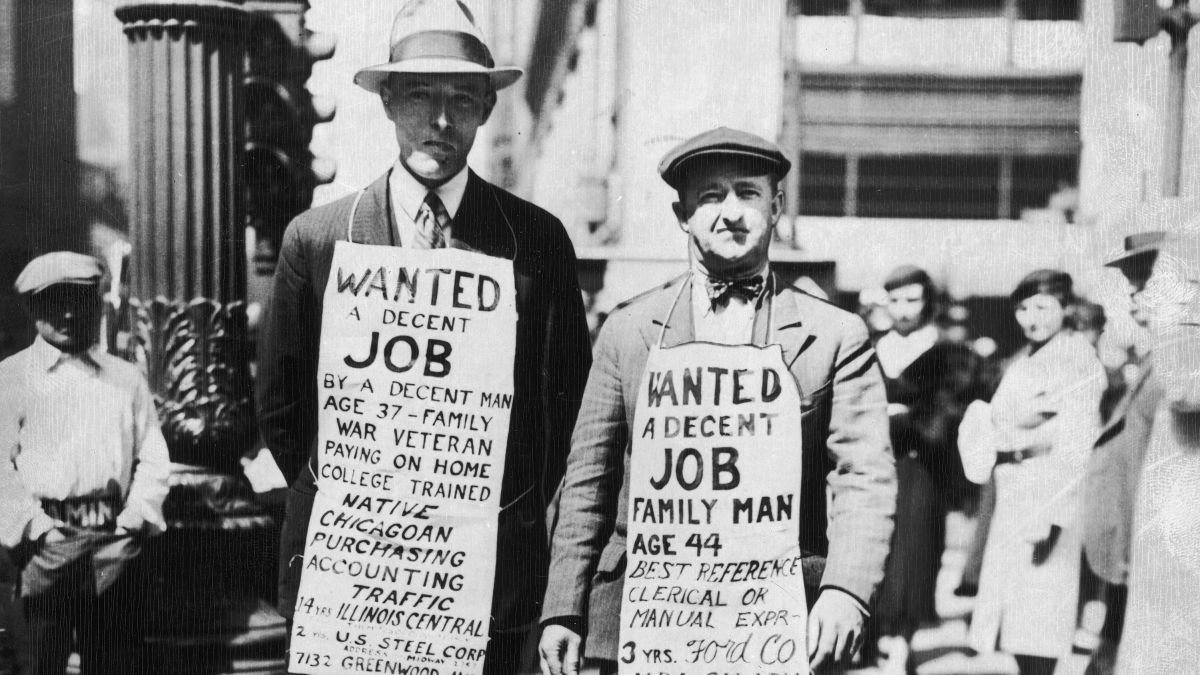

Interestingly, the term “recession” was not used prior to the 1930s. Up until that time, any downturn in the economy was referred to as a “depression” – or worse yet, a “panic”. The term “The Great Depression” was then used to distinguish it from the previous depressions. The term “recession” came into being in the late 1930s when politicians didn’t want people to think incorrect policies were creating yet another depression. So they referred to the new downturn as a more modest sounding “recession.”

Canada’s Last Recession – 2008-2009

In 2008-2009 during the global financial crisis, Canada experienced a significant recession – long and quite deep in terms of decline. Many financial institutions around the world became unstable as a result of investing in assets that quickly lost value, such as real estate in the U.S. Uncertainty exploded, companies cut back, workers were laid off, incomes fell. As a result, spending and demand fell, leading to further declines in production, jobs, incomes and GDP. Actions were taken that thankfully gradually stabilized the global financial system and economic times began to normalize and expand. Consequently, since that time Canada’s economy has consistently grown, expanding each year.

Economies Have Always Gone Through Cycles

That is what economies tend to do – go through periods of expansion and then periods of decline or contraction. We hope the periods of expansion are more lengthy and more positive than the periods of decline – and, for Canada over the last number of decades, that has been the case. We have prospered as a country and as a result our national finances, and our financial institutions, are in solid shape.

Economies Can Expand …

Now to the crux of the matter. Economies expand and grow as demand and spending grow. That is, as incomes grow, people tend to want, and are able, to buy more things. “Demand” or spending in the economy comes from four primary sources – consumers, businesses, government and those who buy our exports. Higher demand leads producers to produce more. This helps create more jobs and incomes, which can then lead to more spending and demand, which can lead to yet more jobs and incomes – and that economic momentum can continue, leading to a period of economic expansion and rising Real GDP.

And Economies Can Contract …

But things can happen to turn the tide and move the economy in the other direction. For example, in the 1980s, for various reasons, inflation became a real problem in Canada, rising to about 12% annually in the early 80s. Inflation erodes the value of our money and high rates of inflation lead to a variety of challenges and issues for many people, especially those who live on fixed incomes. It makes planning for the future difficult. It increases interest rates for borrowing. It leads to a decline in the value of the dollar, making our imports more expensive. And so on. Steps had to be taken to bring inflation down. As a result, interest rates were increased to bring down the level of borrowing and spending. With spending and borrowing levels falling, the economy gathered momentum downwards and went into a period of contraction. Canada experienced a recession.

Periods of Economic Expansion and Contraction = The Business Cycle

The recession was a result of economic events, realities, behaviour and policies that impacted the level of demand and spending in the economy. After the recession and the period of decline, changing economic events, realities, behaviour and policies helped the economy to turn upwards and, consequently, growth and expansion set in again. That is the normal business cycle that most economies experience over lengthy periods of time. During good times, spending, borrowing, production, jobs and incomes increase. During the not-so-good times, spending, borrowing, production, jobs and incomes decline. The normal business cycle, then, has periods of expansion followed by periods of contraction – and we hope the former are longer than the latter.

A Decline of 9% in GDP in Normal Times Would Be Truly Historic – But This is Not Normal

It would truly be extraordinary for an economy to contract by 9% in the normal course of the business cycle. Everyone would have every right to see that as dramatic and terrifying if demand and spending fell off a cliff and sent production levels down that far that fast. But these are not normal times. And this is not a normal part of the business cycle. Production, jobs and incomes are not falling because of an evolving fall-off in demand and spending. They are falling because the economy has been legislated to shut down. Legislation has generated the “supply shock” by enforcing the closing of many businesses and the hunkering down of people in their homes. This has led to layoffs and the loss of jobs and incomes in the fight against this global pandemic.

Important to Compare Economic Apples to Apples

A 9% decline in economic activity in these circumstances is not the same as an economic decline of 9% during normal economic times. The level of unemployment (those who want to work but are unable to find a job) and the level of GDP may well fall to, or even below, Great Depression levels. But, for the reasons described above, things are not the same as they were then. As noted economist and Nobel Laureate Paul Krugman has stated, it is as if the economy has been put into an induced coma. The key question is how we come out of this induced economic coma.

It is true that when the lockdown of business activity is over, the climb back up will be more gradual than was the sharp and rapid decline down. But a considerable amount of economic activity should come back on line quite quickly. Many people will be rehired from layoffs. More jobs and incomes will return. Demand and spending will start to rise. Hopefully momentum will be able to mount on the upside. And hopefully steps that have been taken by governments to try to ease the economic pain and disruption during this period will assist the recovery.

For example, when Air Canada rehires 16,000 workers because of wage subsidies provided by the government that should help the airline restart more quickly when the economy opens up again. It is policies like that, undertaken while the economy is in its coma phase, that should enable the Canadian economy to recover more quickly.

But we should also keep in mind that there will be consequences of the actions being taken by governments to mitigate the downside. Governments will come out of this with very large debt burdens. Interest will need to be paid on the large debts – which means the interest payments will take money away from other possible government programs and expenditures. Governments, in general, will have to cut back on some programs and spending as a consequence of the large debt burdens, and also as they face trade-offs in what they give up to reform and upgrade our health care systems and readiness. The major source of revenue for government is taxes and, with the higher debt burden, taxes will pretty much assuredly rise. And that will likely be the case for middle and higher level income earners. We also have to hope that our efforts can prevent a second wave of infection because governments by that time will be much less able to cushion the blow, having taken the current steps.

This is Not Likely to Be Like The Great Depression

However, challenging as these times are and will continue to be, this is not like the Depression. As we have noted, the economy didn’t gradually slow down; it was legislated into a dramatic nose-dive. When the shutdowns gradually end and restrictions come off, the economy’s nose should pull up out of the dive, Demand, spending, production, jobs and incomes should begin to rise again. The rise may not be as fast as we would like, but the recovery should begin.

Many Things May Change – or Linger

That is not to say that all things will be the same. You can’t have a global event of this scale without an impact. There will be significant and long-lasting changes. Warren Jestin, previously the Chief Economist with Scotiabank, shared some of his thoughts on what we may well see in our future. What are some of those likely outcomes?

- While many may return to their jobs, or secure a new one, unemployment will likely remain high for a longer period, especially in some sectors because the return to full economic activity will be staggered and will affect different sectors of the economy differently;

- Bankruptcies, both business and personal, will likely increase significantly as those that were operating close to their financial edge are not able to recover;

- Some companies will actually benefit from the pandemic – such as those that have effectively shifted activities and operations to an online platform;

- There will be challenges to which Canada will need to adjust, as there were when we struck the free trade agreement with the U.S. and then the U.S. and Mexico. Canada did a pretty good job adjusting and shifting production and employment to new areas of opportunity. Canada will face the same challenge again. We will need to be innovative in our response to a changed world and altered economic structures;

- There will be significant acceleration in some shifts that were already underway – such as shifting to online shopping, working from home, virtual meetings and so on;

- The pandemic will most assuredly lead to a review and reform of our healthcare system and its preparedness for events such as the pandemic;

- We need to recognize that there will be a real income loss experienced in 2020 from the shutdown in production activity and that real income loss will impact individuals, businesses and governments;

- There will be serious and close reviews of our production supply chains to determine how they were impacted and how they could be better protected in the future. This will be particularly true of our transportation networks – trucking, shipping, rail, etc. – which will also be impacted by changing trade relationships and declines in the trade capacity and activity of some of our trading partners;

- Most negatively affected, or slowest to recover, will likely be those in the hospitality and entertainment industries – hotels, restaurants, movie theatres, theatres, etc. They will face higher costs to prepare for the return of audiences and clients and to be able to provide assurance of safety. Their struggles will also affect tax revenues that can impact municipal government revenues;

- Airlines will similarly struggle to gain the confidence of flyers again and will face similarly higher costs to gain trust and provide assurance of safety;

- The incredible increases to government debt will lead to prolonged periods of low interest rates and rising taxes for many;

- The rate of recovery will also be different for different nations. Some, or many, of the developing and emerging economies will likely struggle to deal with both the health challenge and the economic challenge. Some may in fact experience periods of social unrest if governments are destabilized by these dual challenges. Some countries may not have the financial means or systems – such as a healthcare system – to deal with both. Consequently, there may be a widening of the global wealth gap between developed and developing nations – a gap that had been closing in recent years;

- And there will also be a further pushback on globalization as countries seek more control of their own affairs and greater self-sufficiency. There could well be an escalation in protectionism which could dampen global trade just as we are hoping trade will recover. Such nationalistic views may be further influenced by the actions of the United States that have been very U.S.-focused and have done little to enhance global alliances and cooperation.

There are also likely to be some positive outcomes from this tragic time. Such possible outcomes would include, but are certainly not limited to, the following:

- Greater readiness for the outbreak of any such pandemic in the future. But we have to keep in mind that, in addition to the costs incurred by governments at this time, there will be a further future cost to improving our readiness and improving our healthcare systems;

- Greater readiness for other types of social emergency situations as governments improve their readiness, response plans and capabilities;

- Protection and readiness for our healthcare workers should be improved;

- As noted above, supply chains for production should be strengthened;

- Canada should become more self-reliant in terms of some strategic supplies and resources;

- Various levels of government should likely be prepared to respond more quickly and will need to establish means of working collaboratively;

- We will hopefully be better prepared to address the needs of some of those most vulnerable, such as the homeless and those in long-term care;

- The population will, in general, be more skilled in such behaviours as physical distancing, handwashing and general sanitation precautions, and, if required, self-isolation;

- We will hopefully learn from this experience about appropriate policy measures to support the economy, businesses and individuals when faced with such a crisis;

- And there will likely be greater appreciation for the freedoms we have and our family and social relationships, along with possibly more demonstration of compassion towards others as everyone develops a stronger sense of “us all being in this together.”

A Suggested Prescription – Concern, Not Panic

So there is no doubt that times are tough and will be for a while. There will be changes from our previous “normal” – and there is no absolute guarantee that we will not experience times that will come to be called a depression. But we have some good reasons for optimism that we won’t.

No Real Definition of a Depression – But This is Not Likely to Be One

There is, in fact, no commonly-used definition of a depression as there is for a recession, other than general agreement that is a really bad, prolonged recession. The Great Depression went on for quite some time through the decade of the 1930s. Various economic factors led to the Depression – including droughts, poor economic policies, countries imposing trade barriers that slowed global trade and recovery, and so on.

We Have Learned A Lot Over the Years

We have learned a lot since then. And there have been many changes in public policies and government actions since The Great Depression. For example:

- There are a variety of what are called “built-in stabilizers” in our economy now to help when the economy hits a downturn – such as unemployment insurance – that didn’t exist in 1930;

- Governments have learned from mistakes that were made back then and since and have learned how to better support economic activity, as has been demonstrated by the many actions undertaken by our federal and provincial governments to help cushion this time of hardship for individuals, businesses and others;

- The Bank of Canada has learned a great deal over the decades and has talented, experienced people who know how to implement policies and undertake actions to insure our economy and the financial liquidity it needs. And, unlike the 1930s, it knows that this is not a time for tightening monetary policy. In fact the Bank has reduced interest rates significantly.

For these and other reasons, these times are not like those times – and though the numbers may be disturbing, and economic information may strike terror into the hearts of some, we have to always keep in mind the “apples to apples” law when making comparisons. The times are different. The reasons for the economic decline are different. The economic experiences and policies are different. And, unlike in the Depression era, governments are taking unprecedented actions to mitigate the economic hardship. And the recovery will be different when steps are taken to let businesses open again, produce again, hire again and pay incomes again.

And Keeping Hope Always Helps!

So we are not trying to sugar-coat things in terms of where the economy is and where it is going. That would be the wrong thing to do in the case of those who have lost jobs that may not return when the economy begins to open up again. It remains to be seen how much legacy “economic scarring” will be left from this crisis – that is, businesses that won’t reopen and jobs that won’t return. And we have noted a wide variety of impacts that Covid-19 may well have on our society. In the same way that The Great Depression had lifelong impact on some people’s behaviour, this pandemic period may well have similar long-term effects.

What we are saying is that, in economic terms, things are not likely to be as bad as some – and some of the numbers – portray them to be. These are challenging times for sure, but this is not like The Great Depression. Although it won’t be quick and soon, we should have this period in our economic rear-view mirror before people come to call it, in hindsight, a depression. There is no guarantee of that – it’s just that we have good reasons to hope and to believe that will not be the case.

Canada and Canadians will have to be creative, innovative and resourceful in our response. We have shown ourselves up to the challenge in the past. We are showing it today. And there is no reason to think that will not be the case in our future.

By Gary Rabbior,

President, Canadian Foundation for

Economic Education

April 20, 2020